Tero Vesalainen

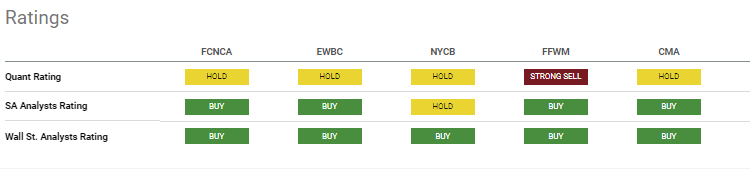

Taking stock of regional banks, Wedbush shifted toward defensive names in the group as the firm expects at least a mild recession in 2024. Analyst David Chiaverini downgraded New York Community Bancorp (NYSE:NYCB), Comerica (NYSE:CMA), and First Foundation (NYSE:FFWM), upgraded East West Bancorp (NASDAQ:EWBC), and added First Citizens BancShares (NASDAQ:FCNCA) to the firm’s Best Ideas List.

First Citizens (FCNCA) “exhibits the characteristics we’re favoring in this backdrop,” Chiaverini wrote in a note to clients. He points to high capital ratios relative to its peers, strong tangible book value growth, expected EPS accretion from its Silicon Valley Bank deal, and attractive valuation.

“We believe capital ratios and TBV will become a bigger focal point of investors in 2024 as credit quality potentially weakens for the bank group, new capital rules are implemented with risk-weighted asset inflation, and the end of the AOCI opt-out for banks over $100B in assets,” he said.

Wedbush upgraded East West Bancorp (EWBC) to Outperform from Neutral on its above-average capital levels, its ability to accrete capital organically at a solid pace, and prospects for growth in tangible book value. EWBC’s CET1 ratio as of Q3 was 13.3% vs. mid-cap median of 11.4%, Chiaverini said.

New York Community Bancorp (NYCB) was cut to Neutral from Outpeform and removed from Wedbush’s Best Ideas List due to is “outsized” commercial real estate exposure, at 47% of average earning assets, in a higher-for-longer rate backdrop, the analyst said.

“We’re concerned with rent-regulated multifamily property economics and office property economics to these borrowers given pressure on debt service coverage ratios as a result of higher rates and work from home,” he said.

Chiaverini cut Comerica (CMA) to Neutral from Outperform on its below-average earnings growth in 2024, with a preprovision net revenue decline of 14% vs. the regional bank median decline of 1%. Its CRE exposure is the second-highest in the regional banking group, representing 23% of its earnings assets as of Sept. 30.

Other factors include its relatively low capital levels, with CET1, adjusted for AOCI, at 5.2% vs. peer median of 7.7%. Even though Comerica (CMA) isn’t subject to the end of the AOCI opt-out on capital ratios, Wedbush worries that investors will apply the potential new rules to banks that are nearing $100B in assets, including CMA at $85B.

First Foundation (FFWM) goes to Neutral from Outperform on the potential for pressure on its net interest margin in Q4 due to rising funding costs. The company’s NIM has declined for four straight quarters before increasing by15 basis points in Q3, a reprieve that may be short-lived. The company also has above-average CRE exposure at 50% of earning assets.

Note that the SA Quant system has no Buy ratings on the stocks mentioned by Wedbush and puts a Sell rating on First Foundation (FFWM). Compare the stocks’ key metrics in SA’s peers tab.

More on Comerica, East West Bancorp, etc.

Image and article originally from seekingalpha.com. Read the original article here.