Apple AAPL is set to report its fiscal Q4 earnings on October 27 as big tech reports continue this week. Still trading 18% from its highs, this earnings release could be critical for the momentum of AAPL stock. While other tech stocks have been hit harder during the economic downturn, Apple has shown some resilience with its broader retail and services capabilities.

Image Source: Zacks Investment Research

Apple’s business has been centered around its flagship iPhone and other products like its Mac computers and iPads. However, diversity and expansion in its paid services have helped boost its top and bottom lines and helped it outperform the Nasdaq over the last year.

Growth in Services

Similar to other big tech giants like Alphabet GOOGL and Amazon AMZN, Apple has continued to innovate. Apple’s iCloud services, App store, Apple Music, Apple Pay, digital content, and licensing have expanded the tech giant outside of its famous product lineup. This also shows Apple has been able to make good use of its $62 billion cash pile.

Investors will want to see if Apple was able to continue growing its services revenue to go along with product sales. Revenue from services was up 12% at $19.6 billion last quarter. This helped the company reach a June quarter revenue record of $83 billion, up 2% year over year. This also made up for product revenue being down -1% last quarter in a tougher operating environment.

During its fiscal Q3 report, Apple generated nearly $23 billion in operating cash flow and was able to return over $28 billion to shareholders. Continued growth in services revenue has helped lift Apple’s operating income during the economic downturn. This could also help sustain the company’s ability to continue innovating, and raise its dividend while keeping an abundance of cash on hand.

Despite the record fiscal Q3 revenue last quarter, AAPL narrowly beat earnings expectations amid challenging operating environments. Investors will hope AAPL continued to lower operating costs during the quarter and produced stronger top and bottom line results.

Fiscal Q4 Outlook

The Zacks Consensus Estimate for Apple’s fiscal Q4 earnings is $1.26 a share, which would represent a 1% increase from Q4 2021. Sales for Q4 are expected to be up 6% at $88.47 billion. Earnings estimates for the period have gone down from $1.31 at the beginning of the quarter but have started to rise again over the last week.

Year over year, AAPL earnings are expected to rise 9% in 2022 and another 6% in FY23 at $6.50 per share. Top line growth is also expected, with sales set to be up 7% this year and another 5% in FY23 to $412.57 billion.

Performance & Valuation

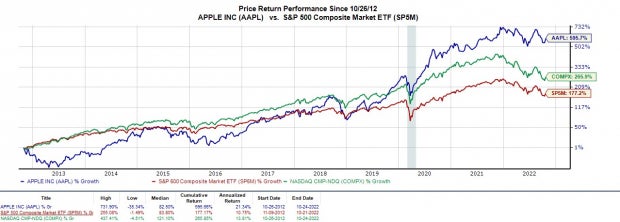

Apple is down -16% YTD to outperform the S&P 500’s -22% and the Nasdaq’s -30%. Even better, over the last decade, AAPL is up +595% to crush the benchmark and the Nasdaq.

Image Source: Zacks Investment Research

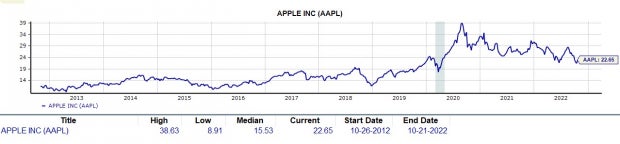

AAPL is still attractively priced considering the stock is two years removed from a 4-1 split in 2020. Trading around $149 a share, AAPL has a forward P/E of 22.6X. This is well above the industry average of 6.5X. However, Wall Street has historically been willing to pay a premium for Apple’s stock for its growth prospects, innovation, and industry dominance. AAPL trades at a discount to its decade-high of 38.6X and is slightly above the median of 15.5X.

Image Source: Zacks Investment Research

Bottom Line

Another earnings beat amid economic uncertainty could be a catalyst for Apple stock and boost investor optimism. Wall Street will be hoping that Apple can improve on its top and bottom lines, along with showing continued growth in its paid services.

AAPL currently lands a Zacks Rank #3 (Hold) and its Computer-Mini computers Industry is in the bottom 4% of over 250 Zacks Industries. However, Apple has shown itself to be an industry leader and this looks poised to continue as the company adapts to the current economic environment.

Investors may want to consider companies with good cash flow and stronger balance sheets to support themselves during economic downturns. Apple fits this bill and does offer an annualized dividend yield of 0.62% at $0.92 per share. And the average Zacks Price target offers 25% upside from current levels.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Apple Inc. (AAPL): Free Stock Analysis Report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.