Netflix NFLX shares have seen a nice rally after beating Q3 earnings expectations by 46% with earnings of $3.10 per share. Sales were up 6% from the prior year at $7.9 billion to narrowly beat revenue expectations. Outside of the beat on both its top and bottom lines, Netflix posted subscriber growth.

Subscriber Growth

Netflix added 2.41 million subscribers during the third quarter. This more than doubled the expected 1.09 million subscribers and was a delight to investors. Netflix’s Asia-Pacific region accounted for the majority of the growth with 1.43 million subscribers added.

Image Source: Zacks Investment Research

Subscriber growth was crucial for Wall Street to see after the company had two consecutive quarters of shrinking subscriber growth. This caused NFLX stock to fall mightily earlier in the year despite beating earnings expectations. The loss of 200,000 subscribers in Q1 was the company’s first decline in paying customers in over a decade. This was followed by another loss of almost 1 million subscribers in Q2 this year.

It is important to note that Netflix said its most recent Q3 release would be the last quarter in which the company provides guidance for its paid subscribers. However, subscriber data will be provided during the company’s quarterly earnings release.

In Netflix’s final forecast the company predicted they would add 4.5 million subscribers in Q4. The company said revenue growth will be its main focus and priority going forward rather than subscriber guidance and data.

Revenue Growth

Netflix’s Q3 revenue was driven by a 5% increase in average paid memberships and a 1% rise in Average Revenue per Membership (ARM). The company also recently announced the launch of its paid advertising subscriptions tier at a lower cost of $6.99 per month. This could help grow its average paid memberships and ARMs. Netflix has implemented the ad-supported service in 12 countries thus far.

The addition of advertising revenue is expected to eventually bring in billions for Netflix. Netflix’s guidance for Q4 has revenue at $7.8 billion with the company saying the forecast is driven by an expectation of 4.5 million paid net adds and ARM growth of 6% year over year. Netflix is optimistic about the new advertising business but doesn’t expect a material contribution in the fourth quarter as the plan is to grow membership in the plan over time.

Although the implementation of advertising subscriptions won’t have a major effect on Q4 revenue, it should eventually put the company in a great position to continue growing and compete for higher ad revenue with big tech companies like Alphabet GOOGL. Alphabet makes billions in revenue from its YouTube ad service alone. To put it in context, Alphabet’s YouTube ad sales of $8.63 billion in Q4 2021 were more than Netflix’s total revenue for the quarter.

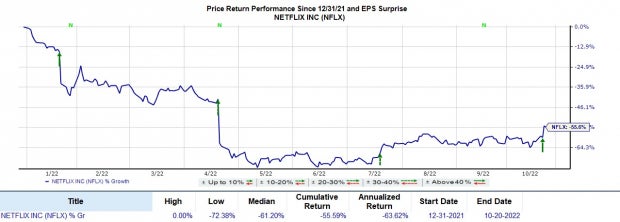

Performance & Valuation

NFLX is up roughly 7% following its solid Q3 earnings release. NFLX shares are still down -59% over the last year to underperform the S&P 500’s -20%. However, over the last decade, NFLX is up a stellar +2,591%.

Image Source: Zacks Investment Research

After the rally, NFLX now has a P/E of 27.2X. This is well below its 65.1X high over the last year and near the median of 25.9X. Even better, NFLX still trades very reasonably compared to its decade-high of 2,640X and the median of 111.9X. Plus, considering NFLX is a stock Wall Street has historically been ok with paying a high premium for; its current valuation is not far from the broader market. Netflix is starting to trade more like the mature tech company it is with its days of 20% or higher revenue growth likely over.

Image Source: Zacks Investment Research

Bottom Line

Netflix’s final guidance on subscriber numbers showed the company should continue growing just at a slower rate than in the past. On top of that, the implementation of its paid ad subscription service could bring billions of additional revenue down the line.

Netflix currently looks poised for near-term growth as well. Year over year, NFLX earnings are now projected to be down -10% in 2022 but climb 8% in FY23 at $10.94 per share. Top line growth is expected, with FY22 sales projected to climb 6% and another 7% in FY23 to $33.90 billion.

NFLX currently lands a Zacks Rank #2 (Buy) with its FY23 outlook showing the company does appear to be growing again. Netflix’s Broadcast Radio and Televisions Industry is also in the top 35% of over 250 Zacks Industries.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.Free: See Our Top Stock And 4 Runners Up

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Netflix, Inc. (NFLX): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.