It’s been a dreadful past several years for shares of Disney (NYSE:DIS), which is actually down 22.9% over the past five years. As the stock looks to recover from seven-year lows on the back of solid quarterly results and optimism over its plan to turn the tides, I’d not bet against the firm as CEO Bob Iger tries his best to bring back the magic in his latest (and probably last) tenure at the company.

Disney may have had many years to turn things around, so you can’t blame shareholders for growing impatient with the firm. That said, I believe patience is vital to making money in such a battered name as it looks to jump above expectations that still seem pretty depressed. For now, I’m bullish and am willing to stick it out with Disney as Iger looks to work his magic.

Indeed, it doesn’t take a lot to surpass estimates whenever the herd expects very little from a firm. We found that out last week as Disney pole-vaulted over analysts’ estimates, causing a nice pop in the stock.

After several brutal years of lackluster performance, Disney is essentially viewed as a “D” student at this juncture. If the firm does enough of its homework, though, it may just be able to score a “B” grade or more. Give Iger another year or two, and Disney may just be able to post several quarters that surprise to the upside for a change. The latest round of better-than-expected numbers may be the first of many.

Disney Stock: Still a Falling Knife, but There’s a Turnaround Plan

Even after the recent post-earnings bounce, DIS stock can still look like a falling knife destined for lower lows to many investors. With macro headwinds facing a firm that’s undergone a “messy” pandemic-era transformation, questions linger as to whether the Disney of the modern era can remain as profitable as the media landscape continues shifting. A turnaround won’t prove easy, but Iger does seem to have the right tools to drag The House of Mouse out of the gutter.

Even in a high-rate world, it’s not just about cost cuts (Disney cut an additional $2 billion in its latest quarter as streaming subscriber growth surpassed expectations). The firm must return to its roots if it wants to bring back the magic. That means spending money in a deliberate fashion to find the optimal balance of growth and margin expansion.

The company’s $60 billion commitment to invest in parks and cruises over the next 10 years, I believe, is a wise move. Disney is head and shoulders above its peers in the amusement industry. And though macro headwinds could weigh down the parks and cruises numbers over the near term, I do think that investing in one of Disney’s key pillars is one way to improve the company’s positioning in a post-slowdown (or post-recession) environment.

As for streaming, Disney was incredibly aggressive in the early days of Disney+ to beckon a wave of new subscribers. Now that the platform has matured a bit, Iger is looking to shift gears into a “building” phase. This new strategy is focused on expanding the streaming service but with an emphasis on profitability and efficiency.

Iger wants to make streaming a profitable business. Given the man’s expertise, I think it’s just a matter of time before he transforms streaming from a “black hole for cash” to one of its most impressive cash cows.

Nonetheless, it seems like the shift to streaming hasn’t been all that bountiful for the legacy media firms, at least compared to the big-tech titans that don’t need streaming to pay off over the near-to-medium term. It also doesn’t help that Netflix (NASDAQ:NFLX) is standing its ground, even as the barriers to entry into the streaming space fall.

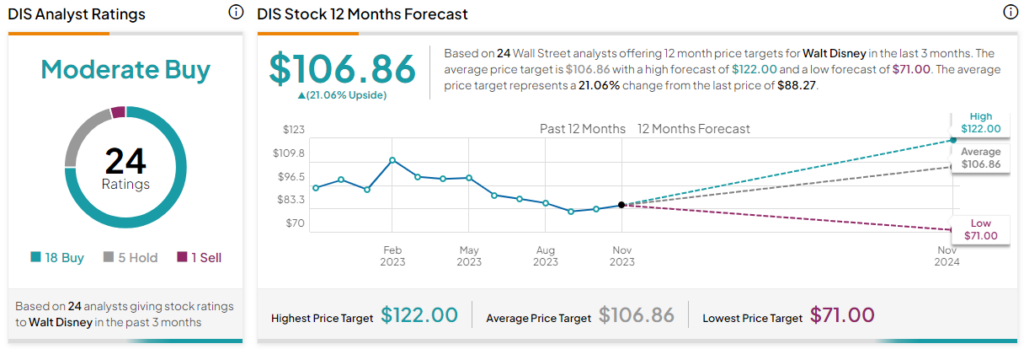

Is DIS Stock a Buy, According to Analysts?

On TipRanks, DIS stock comes in as a Moderate Buy. Out of 24 analyst ratings, there are 18 Buys, five Holds, and one Sell recommendation. The average Disney stock price target is $106.86, implying upside potential of 20.6%. Analyst price targets range from a low of $71.00 per share to a high of $122.00 per share.

The Bottom Line on Disney

Disney certainly isn’t the only media empire that’s under pressure to trim away at expenses of late. But it’s certainly one of the bluest blue chips of the batch and one of the Dow Jones Industrial Average’s biggest dogs.

After a sound Q4, there’s room for hope when it comes to Disney’s turnaround plan. As the economy normalizes, Disney’s job of balancing profitability and growth could be made a whole lot easier.

For now, Disney’s playing the long game. And if activist Nelson Peltz is able to grab a board seat, the stage may very well be set for the stock’s long-awaited recovery, perhaps sooner rather than later.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.