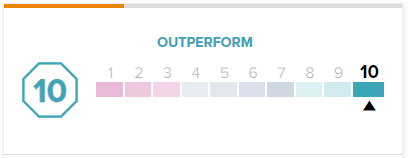

Waste Connections (TSE: WCN) (NYSE: WCN), a “waste collection, waste disposal, transfer, and recycling services” company, has been outperforming the market this year so far. It’s not hard to figure out why -considering it’s a leader in a recession-resistant industry. Notably, the stock has a ‘Perfect 10’ Smart Score while having a Strong Buy rating from analysts. However, do these factors mean you should buy WCN stock now? While WCN may continue outperforming the S&P 500 (SPX) during a bear market, which could make it a decent short-term purchase, it may not be an outperformer when looking a few years out, as its valuation is stretched.

What Makes Waste Connections a Good Company?

No matter what the economy does, people need their trash removed. That’s what makes WCN so predictable, making the stock resilient. Being a large player in a fragmented industry, it has the ability to acquire smaller companies, as it has been doing over the years. In the 12 months ended June 30, 2022, WCN spent US$1.46 billion on acquisitions.

Through acquisitions and organic growth, the company has a 12.8% five-year revenue compound annual growth rate (CAGR), which is impressive for a mature company. Even more impressive, its free cash flow has grown at a five-year CAGR of 16.2% and a 10-year CAGR of 14.5%.

Being an established company also gives it a competitive advantage, as the waste collection business is very capital-intensive. Therefore, it’s not easy for new players to come into the market and challenge WCN. When considering these factors, it’s easy to see why investors like Waste Connections stock.

However, you shouldn’t pay an overvalued price for a business just because it’s good. Let’s take a look at its valuation.

WCN Stock is Not a Bargain in Today’s Market

As we stated above, WCN may underperform in the medium term due to its high valuation. Also, being a low-beta stock, WCN will likely underperform the market when it eventually recovers (which could happen in 2023). At the moment, WCN stock has a P/E ratio of 49.5x and forward P/E ratios of 34.5x and 30x for 2022 and 2023, respectively. While the company is expected to have low-double-digit growth for the next few years, these valuation multiples are usually reserved for high-growth stocks.

Given WCN’s resiliency, we think it deserves a premium, but its valuation is fair at best and overvalued at worst, especially when compared to all the other bargains in the market right now. In addition, WCN has a ~35x price-to-free-cash-flow ratio, which is pretty high, and a low dividend yield of 0.7%.

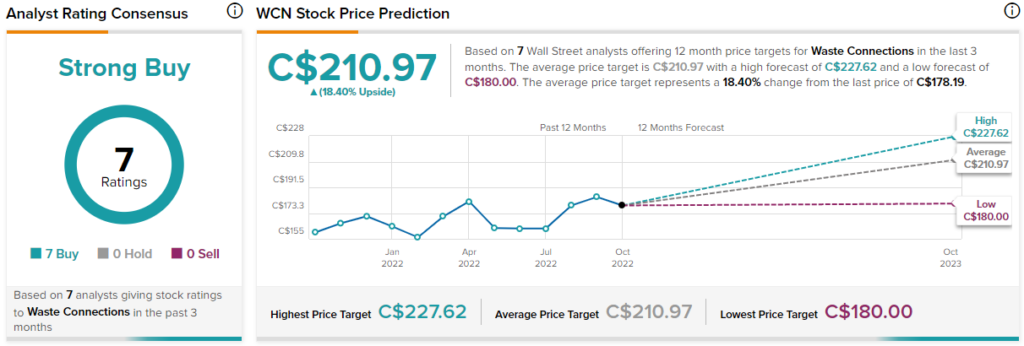

WCN Stock is a Strong Buy, According to Analysts

Turning to Wall Street, WCN stock comes in as a Strong Buy. This is based on seven unanimous Buy ratings. The average WCN stock price target of C$210.97 implies 18.4% upside potential. It seems that analysts aren’t worried about the company’s valuation being relatively high.

Here’s What We Expect from WCN Stock

Waste Connections is a solid performer that will likely continue doing well in the very long term. It should also do relatively well in the short term as long as the market stays in a downtrend. However, in the medium term, as the market (hopefully) recovers, it is likely to underperform for a bit as investors rotate out of safe stocks and into higher-growth stocks, which are likely more undervalued currently. Therefore, we are Neutral on the stock.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.