For investors, having exposure to auto sales has been lucrative with the used vehicle market thriving over the last few years along with the continued expansion of the electric vehicle market.

Of course, Tesla TSLA is a prime example of a top performer in the broader auto industry with its stock up over 1000% in the last five years alone. While every automaker won’t have nearly the same success as Tesla, investing in consumer lending companies that offer exposure to auto loans could be a rewarding option as well.

In this regard, Ally Financial ALLY may come to mind as one of the more well-known automotive finance companies. Another viable option is Credit Acceptance Corporation CACC as the company has the ability to sell vehicles to consumers irrespective of their credit history.

Let’s see if now is a good time to buy either of these automotive finance leaders and get a better gauge of their offerings.

Ally Financial’s Outlook & Auto Finance Overview

Ally is a well-marketed diversified financial services company that provides an array of finance products but derives the majority of its sales from its Automotive Finance Segment.

Operating as a financial holding company (FHC) and a bank holding company (BHC), 45% of Ally’s total earnings assets were from retail auto loans at the end of its most recent fiscal second quarter in July. When including auto leases and commercial auto assets the company’s auto services accounted for 61% of its total assets at roughly $113 billion.

Image Source: Zacks Investment Research

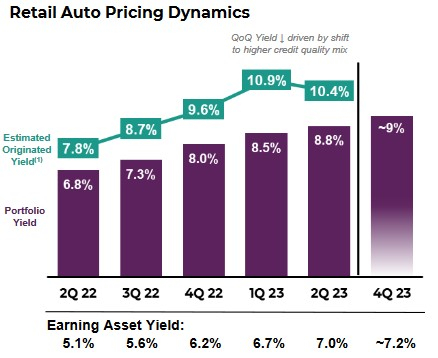

Intriguingly, Ally’s net interest margin has ticked up nicely for its retail auto portfolio which the company expects to hit 9% by the fourth quarter assuming the Fed Funds peak of 5.50% in Q2 with no easing in 2023.

Image Source: Ally Financial

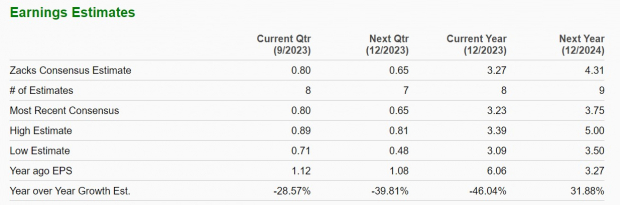

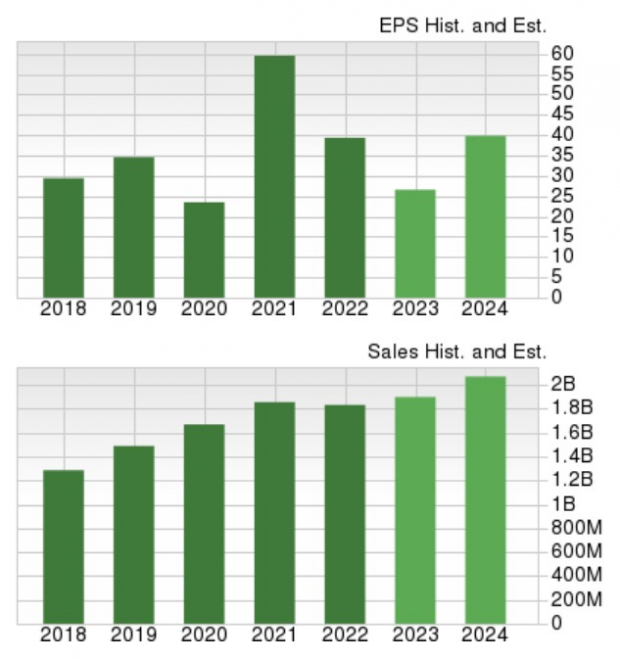

While the rising yield in Ally’s auto portfolio is very promising, the company is up against an extremely tough to compete against year with annual earnings forecasted to fall to $3.27 a share in fiscal 2023 compared to EPS of $6.06 in 2022. However, fiscal 2024 earnings are forecasted to stabilize and climb 32% to $4.31 per share. Total sales are projected to dip -2% this year and then rebound and rise 6% in FY24 to $8.76 billion.

Image Source: Zacks Investment Research

Credit Acceptance’s Outlook & Auto Finance Overview

In regard to Credit Acceptance, its operations are primarily focused on offering financing programs along with related products and services to automobile dealers in the United States.

With a nationwide network of automobile dealers, Credit Acceptance’s bottom line is robust although earnings are expected to drop to $22.78 per share in FY23 compared to EPS of $39.32 a share last year. Still, FY24 earnings are anticipated to rebound and soar 69% to $38.47 per share. Plus, sales are forecasted to rise 4% this year and jump another 9% in FY24 to $2.09 billion.

Image Source: Zacks Investment Research

Recent Performance & Valuation

Notably, Ally’s stock is up 3% YTD and on par with the Financial-Consumer Loans Markets’ +4% although this has trailed the S&P 500’s +15% despite topping Credit Acceptance’s -8%.

With that being said, over the last three years, Credit Acceptance’s stock has risen +26% to top the benchmark and its Zacks Subindustry while ALLY shares have lagged at -9%.

Image Source: Zacks Investment Research

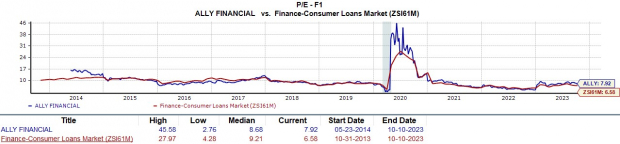

In terms of valuation, Ally’s stock stands out trading at 7.9X forward earnings. This is near the industry average of 6.5X and well below the S&P 500’s 20.4X. Ally’s stock also trades 82% below its decade-long high of 45.5X and at a slight discount to the median of 8.6X.

Image Source: Zacks Investment Research

At a 19.2X forward earnings multiple, investors are paying a premium for Credit Acceptance shares relative to the Financial-Consumer Loans Industry but this is attractively beneath the benchmark. It’s also noteworthy that CACC shares trade below their own decade-long high of 24.4X but above the median of 12X.

Image Source: Zacks Investment Research

Takeaway

Ally Financial and Credit Acceptance certainly have strong prospects as it relates to automotive finance offerings. Furthermore, the P/E valuations of both companies are reasonable at the moment and considering Credit Acceptance’s massive earnings potential its stock currently sports a Zacks Rank #1(Strong Buy) with Ally shares landing a Zacks Rank #3 (Hold).

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.3% per year. So be sure to give these hand-picked 7 your immediate attention.

Credit Acceptance Corporation (CACC) : Free Stock Analysis Report

Ally Financial Inc. (ALLY) : Free Stock Analysis Report

Tesla, Inc. (TSLA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.