With the Internet-Software Industry currently in the top 28% of over 250 Zacks Industries one stock investors will be paying close attention to is PayPal (PYPL) which is set to report its fourth-quarter earnings on Thursday, February 9 and still trades 36% from its 52-highs.

Let’s take a look at what’s going on with PayPal stock heading into the quarterly report.

Overview & Momentum

PayPal stock has rallied of late along with the broader technology sector to start the year on the prospects of easing inflation and a less hawkish fed.

Investors are certainly intrigued by the possibility of more upside for the online payment solutions provider despite increased competition from Alphabet’s (GOOGL) Google Pay and Apple’s (AAPL) Apple Pay among other services such as Block’s (SQ) Square and Cash App.

While PayPal doesn’t have quite the reach as some of the big tech conglomerates, PYPL stock had been a darling on Wall Street in recent years for its specific niche of enabling secure transactions for both customers and merchants with the company also offering peer-to-peer payment services through its Venmo platform.

Furthermore, among the broader technology rally to start the new year, PayPal stock is up +15% year to date to roughly match Alphabet and Apple’s performances and top the Nasdaq’s +13% and the broader S&P 500’s +8% while only trailing Block’s +31%.

Image Source: Zacks Investment Research

Quarterly Estimates

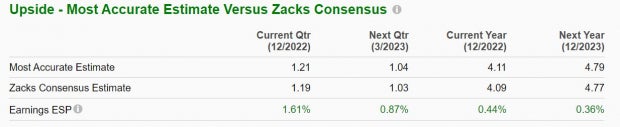

The Zacks Consensus for PayPal’s Q4 earnings is $1.19 per share, which would be a 7% increase from Q4 2021 EPS of $1.11. Also, with the Most Accurate Consensus at $1.21 per share, this indicates that PayPal could beat bottom-line expectations by 1.61%. On the top line, Q4 sales are forecasted to be $7.39 billion, up 7% from the prior year quarter.

Image Source: Zacks Investment Research

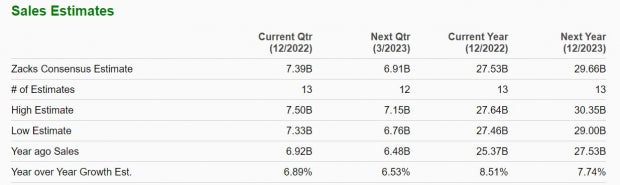

Overall, PayPal earnings are now expected to dip -11% to round out FY22 but rebound and climb 17% in FY23 at $4.77 per share. Earnings estimate revisions have slightly gone up for FY22 but have moderately declined for FY23 over the last quarter. Sales are forecasted to be up 8% for FY22 and rise another 8% in FY23 to $29.66 billion.

More impressive, Fiscal 2023 sales would represent 92% growth over the last five years with 2018 sales at $15.45 billion. This shows that PayPal is still expanding despite increasing competition from Alphabet, Apple, and Block although PYPL’s growth rate is much slower than in the past.

Image Source: Zacks Investment Research

Valuation & Historical Performance

Over the last year, PayPal stock is still down -32% to trail Apple’s -11%, Blocks -20%, and Alphabet’s -26%, and only Apple has outpaced the Nasdaq’s -15% with the majority of tech stocks trailing the S&P 500’s -9%. In the last decade, PayPal’s +123% also lags its closest payment solution competitors as well as the Nasdaq and Benchmark.

Image Source: Zacks Investment Research

Still, after last year’s drop PayPal’s valuation indicates PYPL stock could have a considerable amount of upside. At around $82 per share, PYPL trades at 22.4X forward earnings which is 74% below its decade high of 87.8X and a 49% discount to the median of 44.1X. Plus, this is well below the Internet Software Industry average of 58.3X and closer to the broader S&P 500’s 18.9X.

Takeaway

Although there is increasing competition from other payment solution providers, PayPal still controls the majority of the market and this alone could lead to more upside in the stock as reflected in the company’s solid top-line growth.

With the broader technology sector as a whole still dealing with economic headwinds in correlation with higher inflation and operating costs, PYPL stock lands a Zacks Rank #3 (Hold) as the guidance the company provides in its fourth-quarter report will be crucial to further upside in the stock.

Just Released: Free Report Reveals Little-Known Strategies to Help Profit from the $30 Trillion Metaverse Boom

It’s undeniable. The metaverse is gaining steam every day. Just follow the money. Google. Microsoft. Adobe. Nike. Facebook even rebranded itself as Meta because Mark Zuckerberg believes the metaverse is the next iteration of the internet. The inevitable result? Many investors will get rich as the metaverse evolves. What do they know that you don’t? They’re aware of the companies best poised to grow as the metaverse does. And in a new FREE report, Zacks is revealing those stocks to you. This week, you can download, The Metaverse – What is it? And How to Profit with These 5 Pioneering Stocks. It reveals specific stocks set to skyrocket as this emerging technology develops and expands. Don’t miss your chance to access it for free with no obligation.

>>Show me how I could profit from the metaverse!

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Block, Inc. (SQ) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.