The Zacks Computer and Technology sector has tumbled in 2022 amid a hawkish pivot from the Fed, down more than 30% and widely underperforming the S&P 500.

A commonly recognized name in the sector, Intel Corp. INTC, is on deck to unveil quarterly results on October 27th after the market close.

Intel is the world’s largest semiconductor company and primary supplier of microprocessors and chipsets. Gradually, the company has reduced its reliance on the PC-centric business by moving into data-centric businesses.

Currently, the company carries a Zacks Rank #5 (Strong Sell) with an overall VGM Score of a D.

How does everything shape up heading into the print? Let’s take a closer look.

Share Performance & Valuation

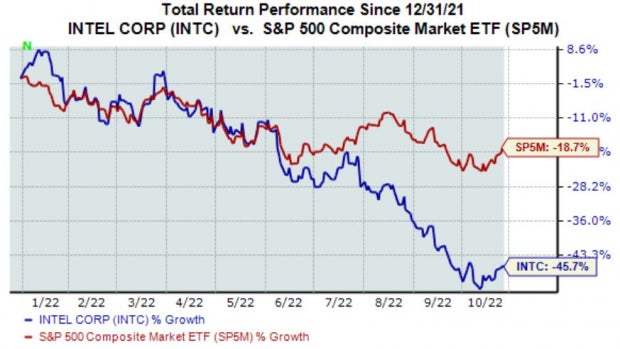

Intel shares have sailed through choppy waters in 2022, down above 45% and coming nowhere near the S&P 500’s performance.

Image Source: Zacks Investment Research

Over the last three months, sellers have maintained a tight grip, with Intel shares down just above 30%.

Image Source: Zacks Investment Research

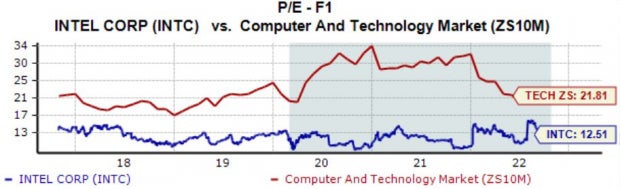

The company’s valuation multiples have pulled back amid the stretch of poor price action; its 12.5X forward earnings multiple reflects a 43% discount relative to its Zacks Computer and Technology sector average and is off 2021 highs of 14.8X.

Still, it’s worth noting that the value is above its five-year median of 12.1X.

Image Source: Zacks Investment Research

Quarterly Estimates

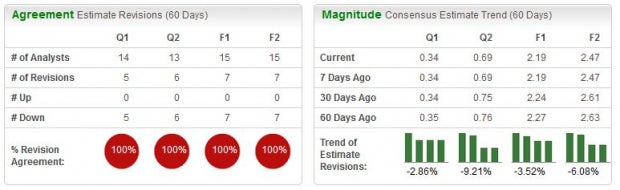

Analysts have been bearish for the quarter to be reported over the last several months, with five negative earnings estimate revisions hitting the tape. The Zacks Consensus EPS Estimate of $0.34 suggests a Y/Y earnings decline of roughly 80%.

Image Source: Zacks Investment Research

Intel’s top-line is also undergoing some turbulence; the Zacks Consensus Sales Estimate of $15.5 billion indicates a 19% decline from year-ago quarterly revenue of $19.2 billion.

Quarterly Performance & Market Reactions

Intel has consistently exceeded earnings estimates, exceeding the Zacks Consensus EPS Estimate in nine of its last ten quarters.

However, its one bottom-line miss came in its latest report, when the chip giant fell short of EPS expectations by nearly 58%.

Revenue results paint precisely the same story; INTC fell short of sales expectations by 14% in its latest print, the company’s first miss out of its last ten. Below is a chart illustrating the company’s revenue o a quarterly basis.

Image Source: Zacks Investment Research

In addition, it’s worth highlighting that the market hasn’t liked what it’s seen from the company; shares have moved downwards following each of its last six quarterly prints.

Putting Everything Together

Intel shares have struggled to find their footing in 2022, underperforming the general market across several timeframes.

The company’s forward earnings multiple sits above its five-year median but nicely below 2021 highs.

Analysts have been bearish in their earnings outlook, and estimates suggest Y/Y declines in earnings and revenue.

The company has a history of posting strong results, but its latest quarter broke a long streak of exceeding estimates.

Heading into the release, Intel INTC carries a Zacks Rank #5 (Strong Sell) with an Earnings ESP Score of -2%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2021. Previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.Today, See These 5 Potential Home Runs >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.