As earnings season fades, one thing remains true – the so-called earnings “apocalypse” didn’t show its face.

Many companies have posted better-than-expected results, helping to push positive sentiment into investors.

Of course, there have been some laggards as well, but the overall bearish sentiment seemed way overdone.

Soon, we’ll hear from Casey’s General Stores CASY on March 7th, after the market close.

Casey’s General Stores operates convenience stores under the Casey’s and Casey’s General Store names in 16 midwestern states.

How does the company shape up heading into earnings? We can use results from a peer, Costco Wholesale COST, as a small gauge. Let’s take a closer look.

Costco Wholesale

Costco reported earnings of $3.30 per share, 3% above the Zacks Consensus Estimate and growing nicely from the year-ago quarter.

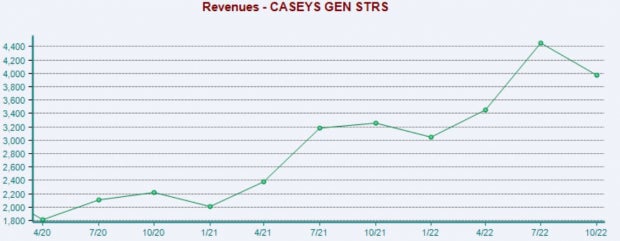

Quarterly revenue totaled $55.3 billion, marginally below expectations and growing nearly 7% year-over-year. Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

In addition, comparable e-commerce sales slipped by approximately 9.6% from the year-ago quarter, but total comparable sales climbed more than 5% year-over-year. And operating income totaled $1.9 billion throughout the quarter, 5% higher than the year-ago quarter.

Further, U.S. comparable sales improved 5.7% year-over-year, and Other International comparable sales also saw a nice boost, climbing nearly 4%.

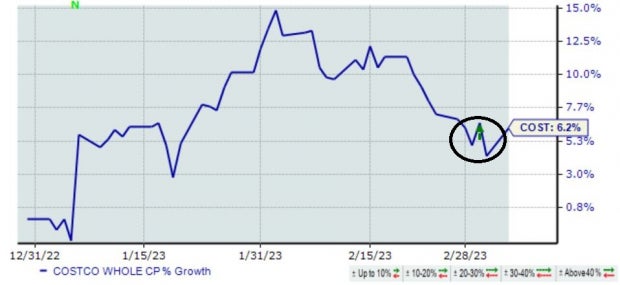

Shares faced selling following the release, as illustrated by the green arrow in the chart below.

Image Source: Zacks Investment Research

Now, onto Casey’s General Stores.

Casey’s General Stores

Quarterly Estimates –

Analysts have been bullish for the quarter to be reported, with three upward earnings estimate revisions hitting the tape over the last several months. The Zacks Consensus EPS Estimate of $1.67 indicates a 2% pullback year-over-year.

Image Source: Zacks Investment Research

Our consensus revenue estimate presently sits at $3.4 billion, suggesting an improvement of more than 10% from year-ago quarterly sales of $3.1 billion.

Quarterly Performance –

CASY has primarily exceeded bottom line expectations, penciling in three EPS beats across its last four quarters.

Top line results have left some to be desired, with the company falling short of revenue expectations in back-to-back quarters.

Image Source: Zacks Investment Research

Valuation –

CASY shares currently trade at an 18.6X forward earnings multiple, beneath the 24.9X five-year median and the Zacks Retail and Wholesale sector average.

Image Source: Zacks Investment Research

Further, the company’s forward price-to-sales presently sits at 0.5X, a tick beneath the five-year median and again below the Zacks sector average.

Image Source: Zacks Investment Research

The stock carries a Style Score of “A” for Value.

Putting Everything Together

Earnings season continues to wind down, with a handful of companies slated to report in the coming weeks.

Needless to say, the feared earnings apocalypse didn’t materialize, with many companies positively surprising investors.

Soon, we’ll hear from Casey’s General Stores CASY. A peer, Costco Wholesale COST, already reported its results, with the company posting mixed top and bottom line results.

Analysts have been bullish for CASY’s upcoming release, with estimates indicating a slight pullback in earnings but an uptick in revenue.

Heading into the release, Casey’s is a Zacks Rank #3 (Hold) with an Earnings ESP Score of 8.3%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2021. Previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Casey’s General Stores, Inc. (CASY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.