A behemoth in the sector, Microsoft MSFT, is slated to unveil quarterly earnings on October 25th after the market close.

The company’s cloud computing operations has witnessed breakneck growth over its last several quarters and will undoubtedly be a focal point of the release.

Let’s take a deeper dive.

Cloud Computing

Microsoft Azure, the company’s public cloud computing platform, is the only consistent hybrid cloud, delivering unparalleled developer productivity and comprehensive, multilayered security.

The company’s cloud operations raked in $20.9 billion in its latest quarter, marginally falling short of estimates. Still, it represented a sizable 10% sequential uptick and an even larger 20% Y/Y uptick.

“In a dynamic environment we saw strong demand, took share, and increased customer commitment to our cloud platform,” said Amy Hood, CFO, on the company’s most recent cloud results.

For the upcoming release, the Zacks Consensus Estimate for the company’s cloud revenue sits at $20.3 billion, suggesting a 3% sequential decrease.

Share Performance & Valuation

Microsoft shares have underperformed the general market by a fair margin in 2022, down nearly 27%, vs. the S&P 500’s decline of roughly 21%.

Image Source: Zacks Investment Research

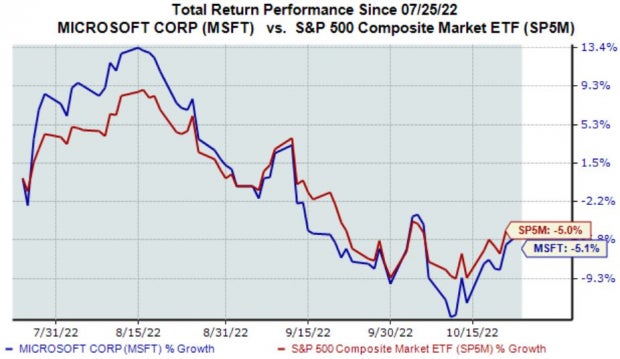

Over the last three months, however, MSFT shares have primarily traded in line with the general market, as shown in the chart below.

Image Source: Zacks Investment Research

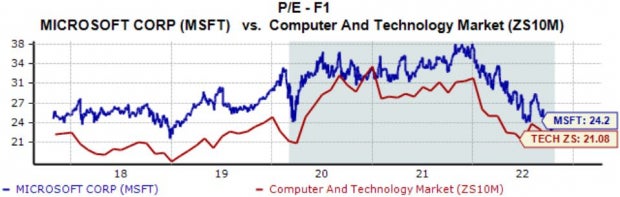

On a relative basis, Microsoft shares are at a cheap price point; the company’s 24.2X forward earnings multiple is well beneath its five-year median of 28.5X and nowhere near 2021 highs of 37.5X.

Image Source: Zacks Investment Research

MSFT carries a Style Score of a C for Value.

Quarterly Estimates

Analysts have been bearish in their earnings outlook, with five negative earnings estimate revisions hitting the tape over the last several months. Still, the Zacks Consensus EPS Estimate of $2.30 reflects a marginal 1.3% Y/Y uptick in earnings.

Image Source: Zacks Investment Research

MSFT’s top-line is forecasted to register growth as well, with the Zacks Consensus Sales Estimate of $49.5 billion indicating Y/Y revenue growth of more than 9%.

Bottom Line

The company’s cloud computing operations have been consistently strong, delivering serious growth. Still, the Zacks Consensus Estimate for the metric indicates a slight sequential decline.

It will be a significant part of the company’s quarterly print, as cloud computing has quickly become a critical technology that an extensive list of companies is shifting toward.

Microsoft has consistently exceeded earnings expectations, with nine EPS beats across its last ten quarters.

However, the one miss out of the previous ten came in its latest quarterly report, when MSFT fell short of earnings expectations by 2%.

Still, it’s worth noting that shares have moved upward following each of its last four quarterly prints, telling us that the market has liked what it’s seen.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.