Earnings season is in full swing.

Investors have been receiving a surplus of quarterly results daily for some time now, with companies finally providing much-needed updates.

And several market titans have already revealed quarterly results.

Now, it’s time for another notable company, Amazon AMZN, to unveil its quarterly results on February 2nd, after the market close.

Amazon has evolved into an e-commerce giant with global operations. The company also enjoys a dominant position within the cloud computing space with its Amazon Web Services (AWS) operations.

How does the company shape up heading into the release? Let’s take a closer look.

Key Metric

As many are aware, Amazon Web Services (AWS) has been a significant growth driver for the company, growing at a breakneck pace over the last several years.

Many will be looking at the Y/Y revenue growth rate in the segment, as many companies have witnessed slowdowns within cloud computing.

Nonetheless, the Zacks Consensus Estimate for AWS net sales stands firm at $21.7 billion, indicating a change of roughly 25% Y/Y.

In its latest quarter, Amazon fell short of our consensus estimate regarding AWS net sales by roughly 1.3%, the second instance in the last six quarters. The chart below illustrates this.

Image Source: Zacks Investment Research

Another player in the cloud computing industry, Microsoft MSFT, has already reported its quarterly results. Microsoft’s Intelligent Cloud raked in $21.5 billion throughout the quarter, exceeding our consensus estimate marginally and growing 18% year-over-year.

Quarterly Estimates

Analysts have lowered their outlook for the quarter over the last several months, with four negative earnings estimate revisions hitting the tape. The Zacks Consensus EPS Estimate of $0.15 suggests a decline of roughly 90% Y/Y.

Image Source: Zacks Investment Research

Our consensus revenue estimate stands firm at $145.4 billion, suggesting a positive change of nearly 6% Y/Y. Clearly, rising costs have impacted the company’s earnings.

Quarterly Performance

Amazon has struggled to exceed bottom line estimates, falling short of the Zacks Consensus EPS Estimate in three consecutive quarters.

Just in its latest release, Amazon fell short of the Zacks Consensus EPS Estimate by roughly 9% and reported revenue marginally under expectations. Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

Valuation

Following a challenging 2022, AMZN’s valuation multiples have pulled back extensively; the company’s forward price-to-sales ratio sits at 1.9X currently, nowhere near the 3.3X five-year median.

Image Source: Zacks Investment Research

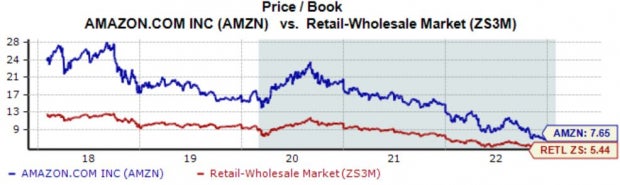

Further, the company’s TTM price-to-book currently works out to be 7.7X, a fraction of the 16.8X five-year median.

Image Source: Zacks Investment Research

AMZN carries a Style Score of “C” for Value.

Putting Everything Together

E-commerce and cloud computing giant Amazon is slated to unveil its quarterly results on February 2nd, after the market close.

Investors will undoubtedly monitor the company’s AWS performance, as it’s been a strong contributor to the top line and a solid growth driver.

Analysts have been bearish in their earnings outlooks, with estimates indicating a decline in earnings but an uptick in revenue Y/Y, a reflection of margin compression.

Further, the company’s valuation multiples have returned to more reasonable levels following rough price action in 2022.

Heading into the release, Amazon AMZN carries a Zacks Rank #3 (Sell) paired with an Earnings ESP Score of -10%.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Image and article originally from www.nasdaq.com. Read the original article here.